Knowledge Center

Making the mortgage process better.

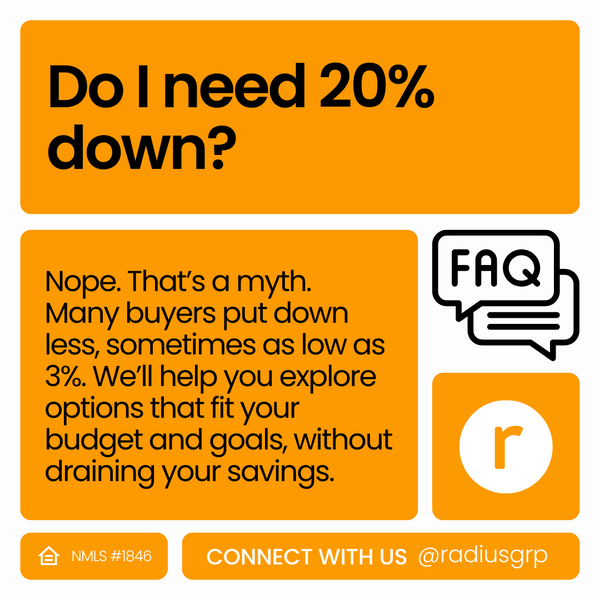

Top 5 Asked Mortgage Questions: 2026 Edition!

Mortgage rates fluctuate based on a variety of economic factors. While no one can predict exact movements, staying informed and understanding your options can help you make confident decisions when the time is right.

Connect with your favorite radius Loan Officer to explore the best timing for your unique situation.

Home values are influenced by market demand, inventory, location, and economic conditions. Even when prices level out, factors like interest rates and affordability still play a role.

Connect with your favorite radius Loan Officer to learn more.

The right time to buy depends on your financial goals, lifestyle needs, and long term plans, not just market trends. A trusted advisor can help you assess your readiness and opportunities.

Connect with your favorite radius Loan Officer to explore the best timing for your unique situation.

From conventional and FHA loans to VA, USDA, and specialized programs, there are financing options to meet many needs. The best choice depends on your credit, income, down payment, and goals.

Connect with your favorite radius Loan Officer to explore the best option for your unique situation.

Refinancing can be a smart move if it lowers your rate, shortens your term, or helps you tap into home equity. It all depends on your goals and current loan terms.

Connect with your favorite radius Loan Officer to explore the best timing for your unique situation.

{kind=link}